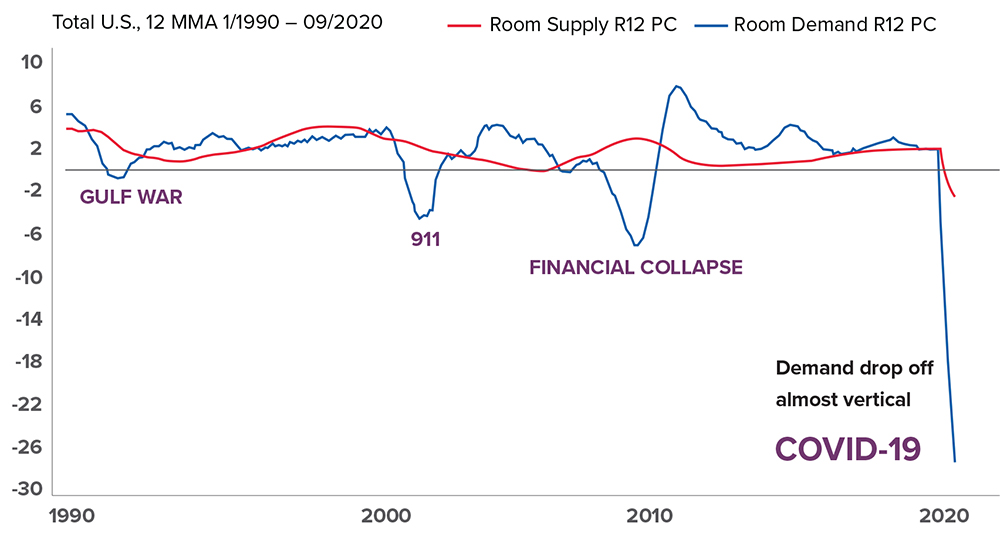

We know that crisis creates opportunity. The chart below describes the relationship between demand for hotel rooms in the US versus large scale events. 911 created a situation whereby the national occupancy average went down by approximately 6%, and the 2008-09 financial collapse created a decrease in room demand of approximately 10%. In relation, the recent pandemic has created a drop-in room demand close to 80% nationally. Given the dramatic decrease in room demand there is no wonder most hotels are struggling with their cash demands and long-term financing, but it also creates the once-in-a- lifetime buying opportunity inside of the sector.

Major International Events + Covid 19

Covid-19 pandemic has dramatically affected the hospitality industry. The industry along with most enterprises in Canada is struggling to adapt to a society with limited mobility and interaction. However, as we see with the US recovery, their hotel room occupancy rate is increasing at an average of 4% week over week (Source: Morning Consult AH&LA). Further, in a study by Marriott International, they have found that over 80% of respondents world-wide intend to travel when restrictions lift.

Inside of the sector we see that hotels which are professionally managed are doing better than those that have single asset managers or ownership teams where hotels are not their core business. We also see that hotels in discretionary markets have fared better than downtown hotels, which is particularly troubling for these locations as they have a much higher cost of developing their amenities such as underground parkades, convention centres, etc.

We believe that buying assets that are well positioned geographically, require an improvement, and can hold a large international brand are the assets that will recover the quickest and provide exceptional returns for our Fund.